Mergers and Acquisition as a strategy for enterprise renewal

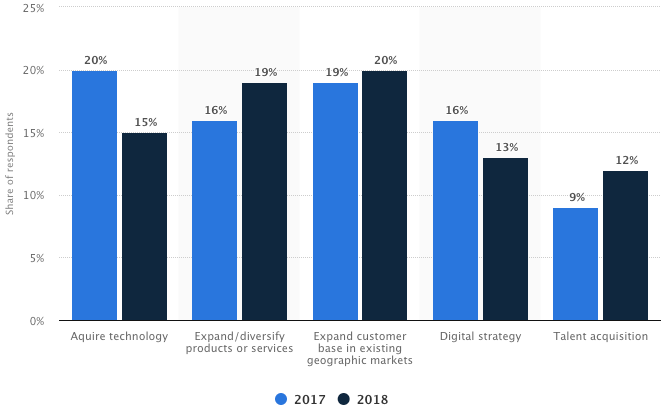

James F. Moore identified that successful businesses evolve rapidly and effectively. Moore also identified companies exist as a part of an ecosystem across a variety of industries (Moore, 1993). The concept of business as a part of an ecosystem suggests that changes to a business can come both internally and externally, resulting in a persistent state of uncertainty about the outcome of decisions. Acknowledging a persistent state of change requires companies to look towards different strategies of evolution to meet the challenge of survival and growth. Merging with or the Acquisition of another company is one such strategy for survival and growth. However, the specific drivers for pursuing Mergers & Acquisitions (M&A) activities are varied, and themselves subject to change, as highlighted in figure 1 below (Cherowbrier, 2018).

Figure 1 2017 vs. 2018 M&A strategic drivers in the United States

The fiscal resources involved in M&A activities are also significant, with the 2018 global value estimated to be 3.9 trillion in U.S. dollars (Szmigiera, n.d.). Interestingly the number of M&A events and the financial resources expended do not necessarily mean that companies have become more effective at achieving successful outcomes. Statistical evidence points to a failure rate of 70 to 90 percent for M&A activities (Gallagher, 2018). Mergers and Acquisitions make for significant investment with a high risk of failure. The drive for competitive advantage and substantial financial investment make M&A efforts a risky proposition.

Risk as a function of Mergers and Acquisitions

The drivers for pursuing M&A are clear. However, just as important to understand are the sources of risk. Examples of risk include: buying an overvalued company; clash of corporate cultures; loss of talent; and failure of the acquiring company to understand the business (or market) they are buying (Connell Curtis Group, 2012). Considering the drive for a business to adapt and self-renew or otherwise die (Moore, 1993), careful planning and analysis must occur. Careful planning and analysis are especially true during due diligence assessments which evaluate factors between both the acquiring and target company around operational, financial, and regulatory elements (DePamphilis, 2019). Bernard (2016) makes a special note to highlight the role of culture in M&A activities and how it is often overlooked or ignored. However, it must be made clear that Merger and Acquisition as terms are sometimes used interchangeably or in concert with one another, but represent different outcomes. The type of M&A effort can change the nature of the risk and who must manage it.

A merger involves two or more entities combining in such a way that previously recognized legal entities cease to exist. The merging entities have a shared burden in defining the new or changed business model; changes in their go-to-market strategy; customer journey, etc. This includes the complexity of the risks involved in getting the necessary clearance and support required in clearing a myriad of regulatory hurdles. All of this means risk and resource allocation decisions above and beyond the typical day to day business operations. Merging companies share an interest in articulating organizational structure and behavior from a strategy, operational, regulatory, and financial perspective.

For Acquisition, the balance of sharing risk and resource allocation shifts depending on the nature of the purchase. In a friendly acquisition, it could look more like a merger in which parties are sharing some level of risk and resource decisions. Both participating organizations have an interest in representing their companies in the best possible light, but perhaps for different reasons. The acquiring firm wants to ensure they can demonstrate to the market and shareholders they are doing the right thing and will bring increased value. The target company, of course, is representing their shareholder and own self-interests. The target firm, possibly, does not give the same level of due diligence or preparation. They may only be looking for the success of the deal itself, and less about follow on implementation challenges. In a hostile situation, the burden is undoubtedly on the acquiring firm.

The definition of risk, in this paper, is defined as the effect of uncertainty that could have a positive or negative impact on objectives. Uncertainty can be around events (occurring or not occurring), ambiguity, or even a lack of information. M&A activities for both the acquiring or target company are high-risk undertakings that are resource-intensive and may not deliver the intended promises to either company, stakeholders, or shareholders. The historical rate of failure requires the exploration of a new approach for improved M&A decision making.

Enterprise Architecture as a means of risk identification

Three key tasks of practicing enterprise architects are to reduce ambiguity; apply creativity, and manage complexity (Crawley, Cameron, & Selva, 2016). These tasks, when done, go to the very heart of helping to reduce risk around the issue of uncertainty. However, it is critical to define 'what is' EA. Bernard (2012) provides the following definition for Enterprise Architecture (EA) as:

“The analysis and documentation of an enterprise in its current and future states from an integrated strategy, business, and technology perspective.”

The above definition provides a broad boundary going beyond the conventional perception of EA as being an Information Technology practice. Enterprise Architecture, as a practice, is about improved coherency management (Doucet, Saha, Bernard, & Gøtze, 2009). Improved coherency management means understanding how a business and its constituent parts inter-operate as well as intra-operate with other companies as a part of a broader ecosystem. Bernard’s definition is also useful in identifying that EA practitioners must be capable of conducting analysis and provides a clear delineation from the practice of developing documentation (e.g., models) alone.

The Line of Sight (LOS) model (Office of Management and Budget, U.S. Govt. , 2013) provides a concise means of articulating the contributions of holistic EA to enterprise visibility. This model, as depicted in the middle of figure 2, provides a method of highlighting traceability of asset(s) to an outcome(s). Internally, the LOS artifact allows for self-evaluation about which assets bring direct value and how they contribute to the organization's market value. Externally, the LOS model provides a means of exchanging detailed information about how INPUTs (e.g., Human Resources, Information Technology, Fixed Assets, and Financial Assets) support operational activities that are measured as leading indicators and finally the results as strategic outcomes.

Figure 2 EA frameworks coupled with Line of Sight model allow for enterprise traceability and intelligence

The LoS model used in conjunction with the EA3 cube framework (Bernard, 2012) provides a means of normalizing understanding between two different companies as represented by Company A & B in figure 2. As information is received and decisions are made, the LOS artifact can be quickly updated. Rapid Instantiation allows for improved understanding, which reduces ambiguity, allows for increased creativity around how companies might merge or what could be spun off as a part of an acquisition, etc. Finally, the understanding between company operations, finance, and compliance impacts allowed for a more clear understanding of corporate culture fit and increased complexity management capability. The factors listed above go directly to the reduction of uncertainty and provides value to M&A activities as a function of reducing the risk resulting from uncertainty.

Bibliography

Bernard, S. (2016). Organizational Design & Architecture for Mergers & Acquisitions [Carnegie Mellon University Video Lecture]. Retrieved October 7, 2019, from https://scs.hosted.panopto.com/Panopto/Pages/Viewer.aspx?id=1f04707c-6479-42c1-9013-aab001009c79

Bernard, S. A. (2012). An Introduction to Enterprise Architecture: Third Edition [Apple Book] (Rev. ed.). Bloomington, Indiana: AuthorHouse.

Cherowbrier, J. (2018, December 19). United States: strategic drivers for M&As 2017 and 2018 | Statista. Retrieved October 7, 2019, from https://www.statista.com/statistics/950674/united-states-strategic-drivers-for-mergers-and-acquisitions/

Connell Curtis Group. (2012). Business Growth Consulting: The Importance of Mergers and Acquisitions | Connell Curtis Group. Retrieved October 7, 2019, from http://www.connellcurtis.com/business-growth-consulting-the-importance-of-mergers-and-acquisitions/

Crawley, E., Cameron, B., & Selva, D. (2016). System Architecture: Strategy and Product Development for Complex Systems. Hoboken, New Jersey: Pearson.

DePamphilis, D. (2019). Mergers, Acquisitions, and Other Restructuring Activities [Kindle] (Rev. ed.). London, United Kingdom: Elsevier Science & Technology.

Doucet, G., Saha, P., Bernard, S., & Gøtze, J. (2009). Coherency Management: Architecting the Enterprise for Alignment, Agility, and Assurance. Bloomington, Indiana: AuthorHouse.

Gallagher, S. (2018, April 17). Increasing The Odds Of Success In A Merger. Retrieved October 7, 2019, from https://chiefexecutive.net/increasing-odds-success-merger/

Moore, J. (2014, August 1). Predators and Prey: A New Ecology of Competition. Retrieved October 7, 2019, from https://hbr.org/1993/05/predators-and-prey-a-new-ecology-of-competition

Office of Management and Budget, U.S. Govt. . (2013). Federal Enterprise Architecture Framework Version 2. Retrieved from United States Federal Government, Office of Management and Budget. (2019). Federal Enterprise Architecture Framework Version 2. Retrieved from https://obamawhitehouse.archives.gov/sites/default/files/omb/assets/egov_docs/fea_v2.pdf

Szmigiera, M. (n.d.). Value of M&A deals globally 1985-2018 | Statista. Retrieved October 7, 2019, from https://www.statista.com/statistics/267369/volume-of-mergers-and-acquisitions-worldwide/

Author: Cort Coghill

Author: Cort Coghill

Dr. Cort Coghill is the director for education operations at the FEAC Institute. In this role, he works with hundreds of enterprise architects every year helping them to help solve a broad variety of problems facing their enterprises. He speaks at different conferences and classrooms around the world every year. His experience includes prior service in the United States Navy, United States Civil Service and as Senior Researcher and Program Manager for the Battelle Memorial Institute. He is passionate about education and research in the field of enterprise architecture and systems engineering. His dynamic speaking style and engagement with audiences helps to make material and the learning experience accessible to his audience.